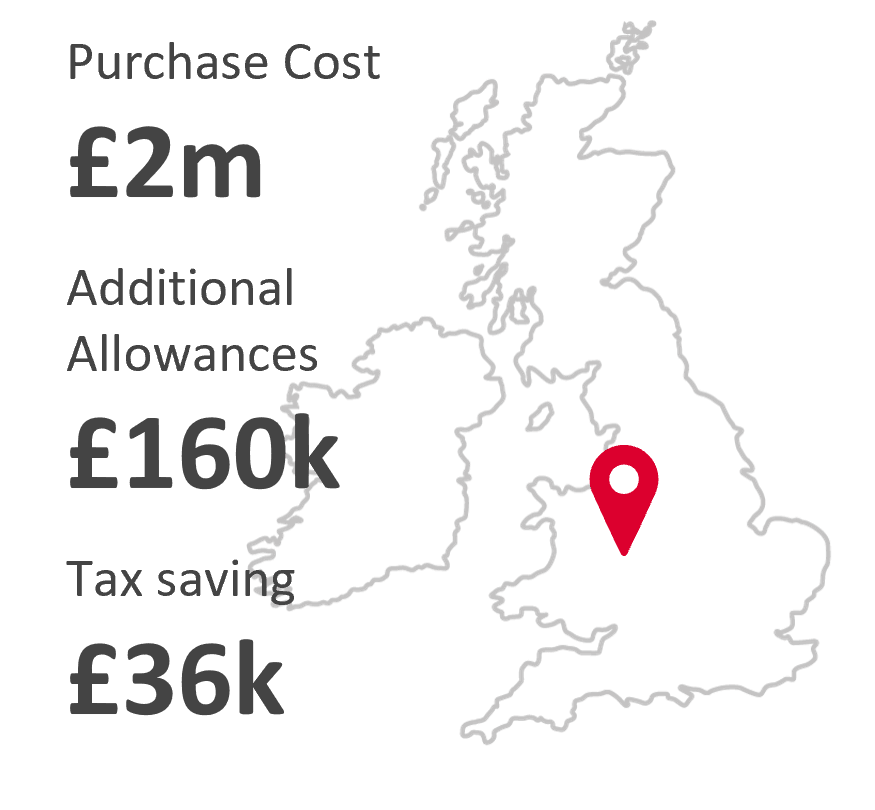

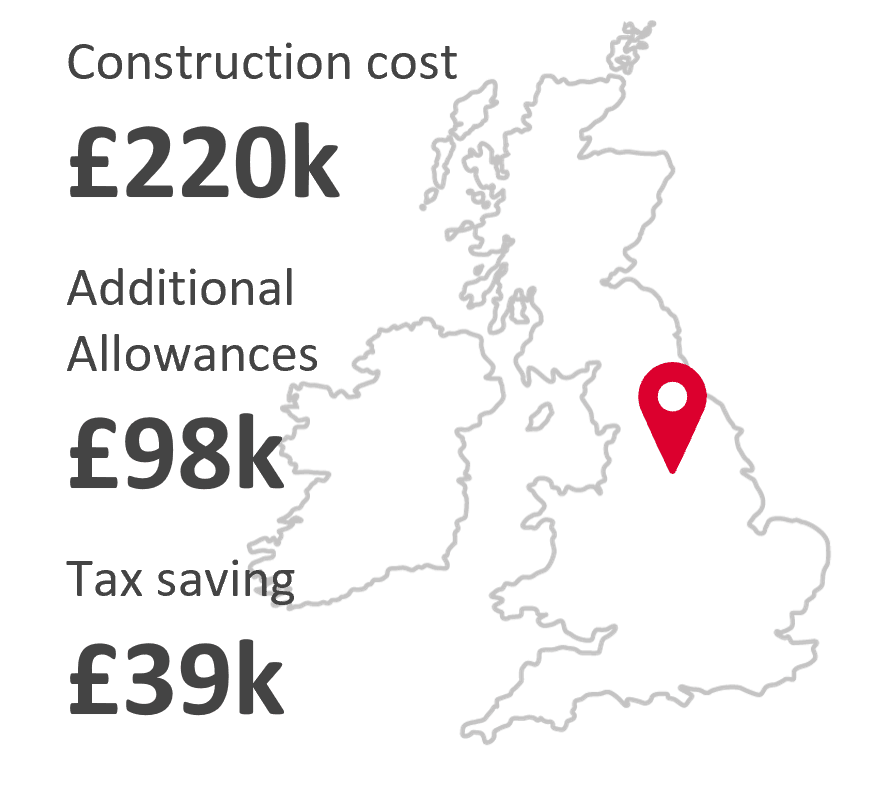

What we did

We re-analysed the whole of the £220,000 of expenditure and identified £98,000 of plant & machinery additions, which was agreed by HMRC without further enquiry. We agreed that no revenue deduction was permitted.

Prior to the enquiry, our client had claimed £88,000 (£44,000 as revenue plus £44,000 as plant & machinery) which had been rejected by HMRC. Annual Investment Allowance was available on the £98,000, resulting in a reduction to tax payable as a consequence of us defending the enquiry.