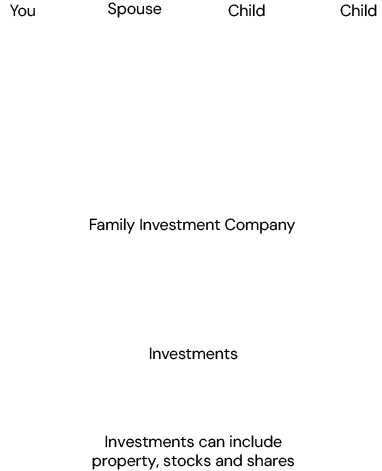

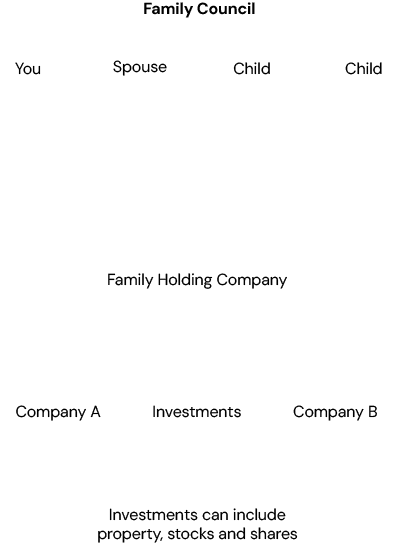

Family Investment Companies (FICs) can be used specifically to accommodate your family’s wealth planning needs in a tax efficient way.

FICs are structured around shares which are distributed to each family member. Different shares can have different voting rights. This offers the option for ownership to be separated from control. Assets such as money, property and investments can be distributed whilst parents or grandparents retain control through their director shareholder position.

// Inheritance Tax (IHT) doesn’t apply. Gifts of shares or cash invested in a FIC made to an individual aren’t usually subject to an IHT charge. So, this structure is effective for those who have maximised their nil rate band.

// Lower rate of tax on dividends. A FIC is structured as a company, and so any shareholders can receive dividends. Each person is taxed individually at a rate dependent on their tax bracket.

// Dividends received by the FIC are usually tax free. Whilst FICs are subject to corporation tax there may be no tax on dividend income. Additionally, shareholders can benefit from a tax-free allowance.

// Corporation tax is lower than income tax. Any other income in your FIC (such as interest) will be subject to corporation tax instead of the maximum income tax rate.

// Director shareholders are established. Director shareholders can benefit from the assets and profits whilst retaining control of the other shares.

// A lower rate of income tax. When shareholders receive income, they will have to pay income tax at their marginal rate. This happens after they have used up their dividend allowance.

// Employer pension contributions can reduce CT liability. FICs can use surplus cash to make employer pension contributions for directors or employees. These contributions will be deductible when calculating the FICs corporation tax liability.