Changes introduced from 1 April 2021

R&D tax credit limited to £20,000 + 3x total PAYE+NIC liability of the company for the year. (Related party PAYE+NIC liabilities attributed to the R&D can be included within the CAP.)

The claim is not capped:

• If the R&D tax credit is less than £20,000.

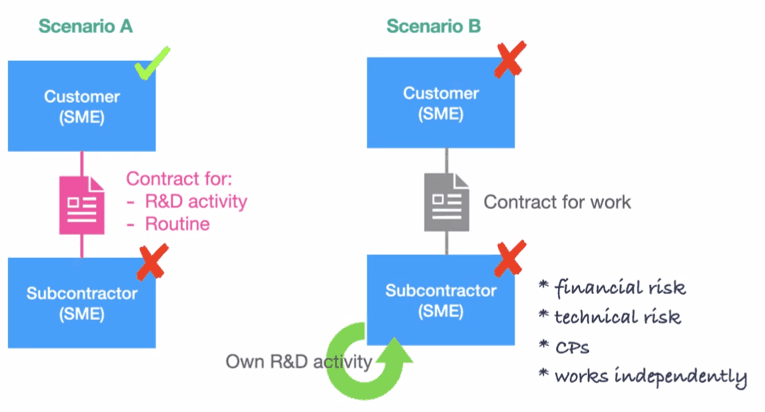

• If the R&D claim meets the following two tests:

a. The company’s employees are creating, preparing to create or actively managing intellectual property arising from the R&D project.

b. Its expenditure on work subcontracted to, or externally provided workers provided by, a related party is less than 15% of its overall R&D expenditure.

Many genuine SME claims will be affected:

• Companies outsourcing large parts of their R&D projects.

• Companies where consumables or software form a large proportion of their R&D costs.