Image copyright James Newton

The Architectural Activities industry involves designing and planning for buildings, urban areas and landscape. Industry demand is heavily affected by trends in construction activity.

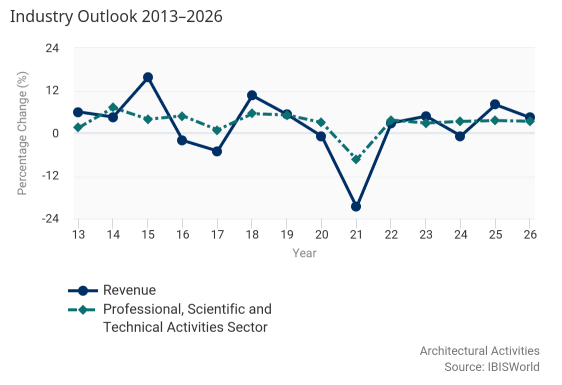

Residential construction activity has been resilient over the majority of the past five-year period, aided by government initiatives introduced to stimulate the housing market and resilient consumer spending, particularly over 2017-18. However, commercial construction activity has fared worse amid lower business confidence and uncertainty following the EU referendum.

Intense competition from multidisciplinary building and engineering firms has put pressure on operators and restricted demand.

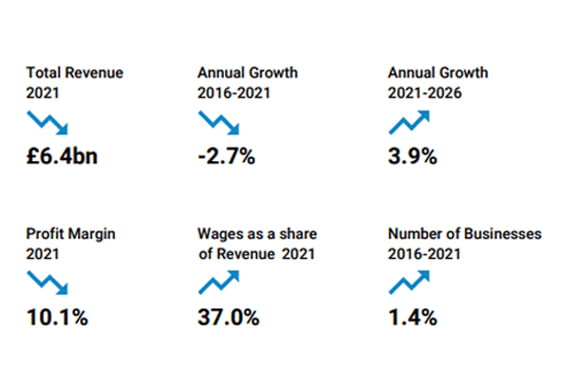

Industry revenue is expected to fall at a compound annual rate of 2.7% over the five years through 2020-21 to £6.4 billion, largely due to a sharp decline in revenue in the current year.

In 2020-21, industry revenue is forecast to drop by 20.7% due to the economic shock of the COVID-19 (coronavirus) pandemic and restrictions throughout the year, which have significantly disrupted construction activity. Data from the Office for National Statistics showed a record decline in new work orders in April 2020, and new work orders were 8% lower in December 2020 compared with February 2020. Construction output fell by 12.5% over 2020.

As architects are mainly required during the initial design stages of construction projects, the volume of new orders is indicative of industry demand. Falling demand from the disrupted construction sector and rising operating costs are anticipated to cause the average industry profit margin to drop to 10.1% in 2020-21.

Over the five years through 2025-26, industry revenue is forecast to increase at a compound annual rate of 3.9% to reach £7.8 billion. The planned easing of restrictions as the vaccination rollout continues is expected to aid economic recovery, although low confidence is likely to subdue investment in construction in the short term.

Nevertheless, commercial building construction is forecast to pick up as confidence grows and investment increases. Moreover, government initiatives are anticipated to support residential building construction.

Over the five years through 2025-26, industry revenue is forecast to increase at a compound annual rate of 3.9% to reach £7.8 billion.

Industry overview provided by IBISWorld.

IBISWorld provides trusted industry research on thousands of industries worldwide. Their in-house analysts leverage economic, demographic and market data, then add analytical and forward-looking insight, to help organisations of all types make better business decisions.

Visit the Ibis website here